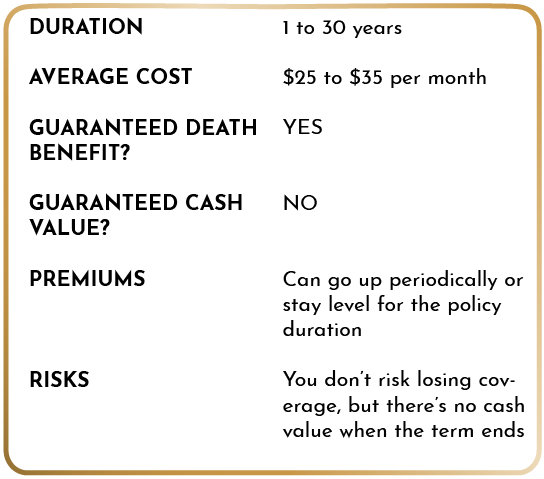

Term life and whole life insurance each have their benefits and drawbacks, and the right choice for you will depend on your circumstances and budget. It’s not a one-size-fits-all scenario, but we can help you figure out which type is best for you.

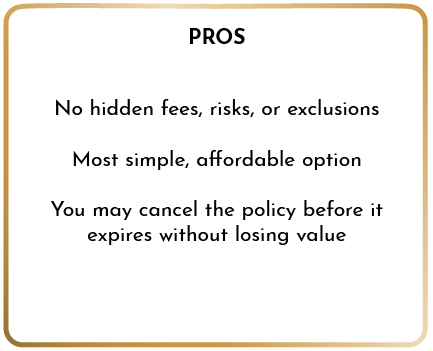

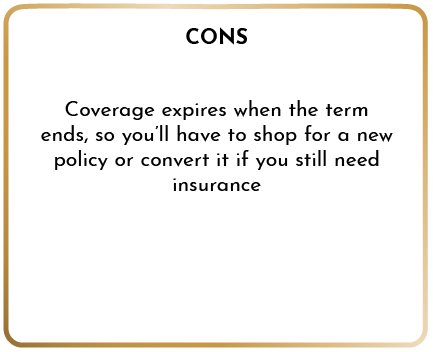

The majority of people shopping for life insurance need affordable coverage for a certain period, which is what you get with term life. If you’re on a budget and want to leave behind a death benefit to cover living expenses, term life is right for you.

On the other hand, if you’re protecting an inheritance that will be prone to an estate tax, want to build cash value, or have long-term dependents, whole life is right for you.