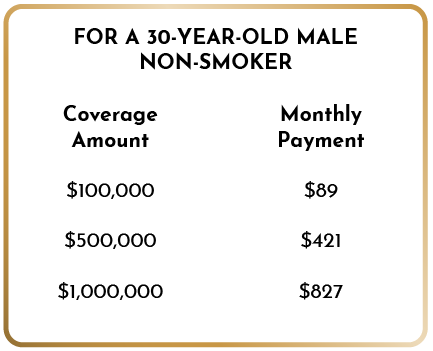

The average cost of permanent coverage is $55-135 per month — much more expensive than a term life insurance policy with the same benefit amount. Whether you buy term life or whole life, your premiums will vary. They’re based on your health, age, coverage amount, term length, and riders you add (but some riders are FREE). The longer your life insurance policy lasts, the more it costs. The more coverage you get, the higher your life insurance premiums will be.

Medical concerns raise the cost of your premiums, and the older you get, the riskier you are to insure. Life insurance rates go up by 4.5-9% each year. Knowing this in advance will help you to not overestimate your ability to pay premiums year after year.